Sponsored by: CanCambria Energy. European gas supply remains constrained, with pricing consistently above North American benchmarks. CanCambria is targeting this gap with a large-scale tight gas project in southern Hungary. Access our Exclusive Investor Report on CanCambria Energy.

For most of the twentieth century, the geography of natural gas was relatively predictable. The countries that sat on the largest reserves, such as Russia, Iran, and Qatar, held structural leverage over the countries that needed the fuel to run their economies, and pipelines were built to reflect that dependency.

That geography is being redrawn. Russia's invasion of Ukraine, a decade of underinvestment in European domestic production, and the rapid scaling of North American LNG export capacity have produced a global gas market that looks fundamentally different from the one that existed just a few years ago. The data below sets out who produced and consumed gas in 20241, alongside 2025 production estimates2, and the regional balances that result. Which routes can move that surplus gas to regions that need it is now a central question in global energy policy.

#Natural gas production and consumption by region

All figures in bcm.

Region | Production 2024 | Production 2025 (est.) | Consumption 2024 | 2024 balance |

North America | 1,263 | 1,362 | 1,131 | +132 surplus |

Middle East & Africa | 978 | 997 | 771 | +208 surplus |

Asia Pacific | 708 | 745 | 973 | -265 deficit |

Russia & CIS | 813 | 843 | 616 | +197 surplus |

Europe | 198 | 198 | 469 | -271 deficit |

Latin America | 165 | 197 | 169 | -4 deficit |

Sources: Energy Institute Statistical Review of World Energy 2025 (2024 data)1; OPEC Annual Statistical Bulletin 2026 (2025 estimates)2. Production excludes gas flared or recycled.

#Five Things Investors Should Know

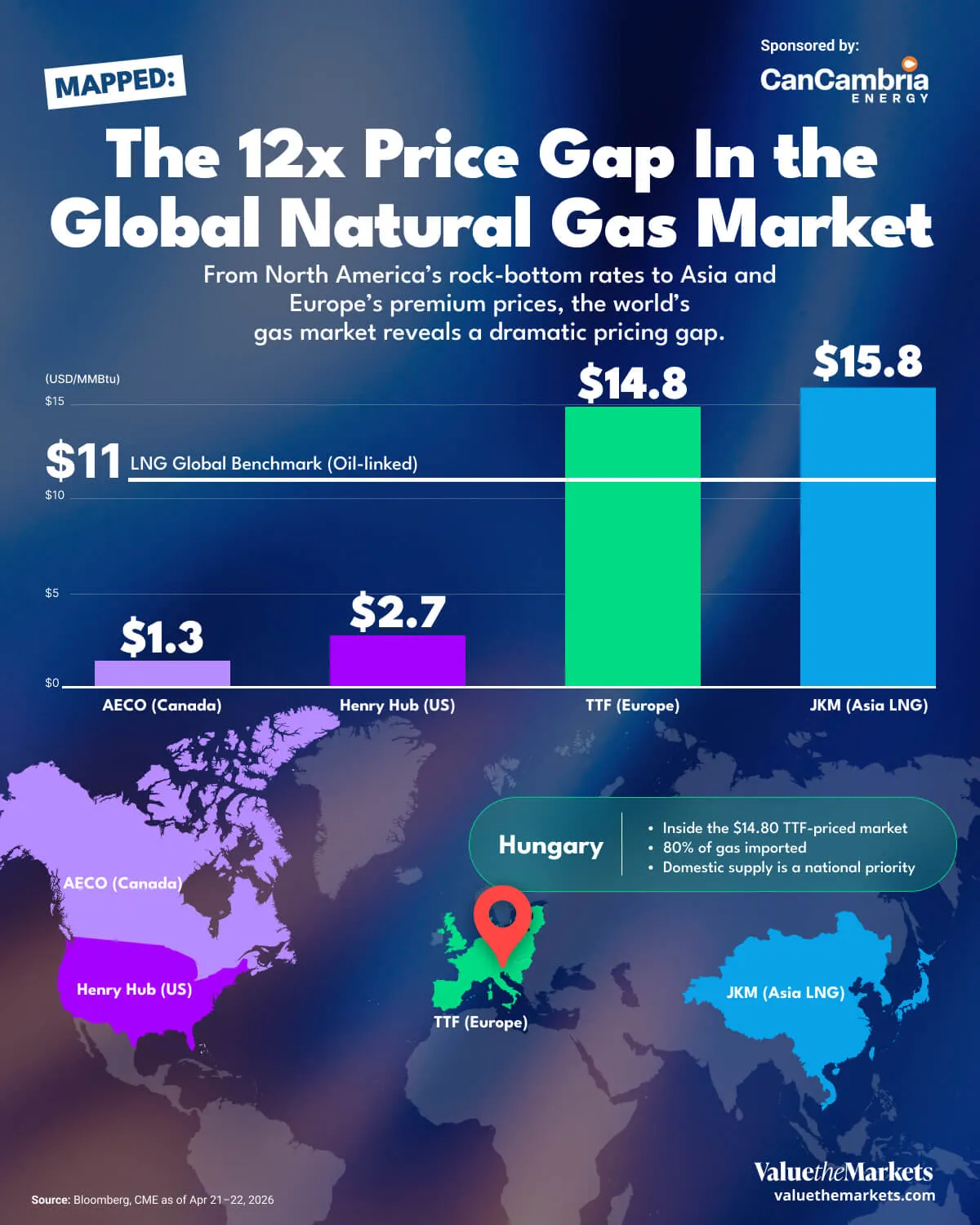

Europe runs the world's largest regional shortfall, producing around 198 bcm (billion cubic meters, the standard unit for gas volumes) in 2024 while consuming close to 469 bcm1. The 2025 estimates show European production flat, so the gap persists2.

The EU has committed to phasing out Russian LNG from January 2027 and Russian pipeline gas by autumn 20273, which makes filling Europe's deficit more politically constrained and increasingly exposed to LNG market pricing.

Asia Pacific is the largest demand center in the world, consuming 973 bcm in 2024 against production of 708 bcm. Europe and Asia compete for the same pool of global LNG supply, so a cold winter or supply outage in one region bids up prices in both.

North America's surplus widened further in 2025 as US shale output expanded, and the infrastructure to move gas to European and Asian buyers already exists. Russia and CIS held a larger nominal surplus in 2024, but most of it has no viable route to premium-priced markets.

For investors, the significant point is that this geography is slow to reverse. Pipeline infrastructure takes decades to build and political relationships take years to rebuild, which makes the data a lens for judging which producing regions are structurally advantaged over a multi-year horizon rather than a short-term trade.

#Why Existing Surplus Regions Cannot Fill the Gap Alone

LNG has absorbed much of the adjustment since 2022. US exports surged as new terminal capacity came online, and European buyers paid the premium required to pull cargoes away from competing Asian demand. But LNG depends on liquefaction at the export end, regasification at the import end, and a global supply pool large enough to service two major deficit regions simultaneously. Recent disruptions to Qatari LNG flows illustrated how quickly those conditions can fail to hold4.

The Middle East and Africa hold the second largest surplus in the data, yet converting it into deliverable supply requires LNG capacity that is capital-intensive, slow to permit, and concentrated in a small number of terminals.

That leaves North America, with growing output, private-sector discipline, and export infrastructure that already works, as the region with the clearest structural advantage among exporters. Yet every molecule of imported supply carries a cost floor set by liquefaction and shipping, which means the other structurally advantaged position belongs to producers operating inside the deficit region itself.

#Producing Inside the Deficit

CanCambria Energy Corp (TSXV: CCEC) (OTCQB: CCEYF) (FSE: 4JH) is advancing its 100%-owned Kiskunhalas tight gas project in southern Hungary. The project is positioned in a European gas market where prices have historically exceeded those in North America, while domestic production meets only around 20% of Hungary's gas demand5. An independently evaluated 2C contingent resource in the Pannonian Basin underpins the project, supported by historical wells, modern seismic, and legacy production data6.

In June 2026, the company announced that technical due diligence had been completed by prospective strategic partners and that commercial negotiations are underway, marking meaningful progress in the joint venture process led by Raiffeisen Bank International7. The farmout targets up to a 50% interest in the Kiskunhalas license to fund an initial drilling program. Subject to completion of the JV process, the company anticipates drilling could commence in Q1 2027, with first gas production targeted for mid-2027. Independent consultancy CHPE assigned a risked NPV10 of approximately US$1.76 billion to the Phase 1 development, based on a January 2025 price forecast and subject to execution, pricing, and cost assumptions6.

"Europe is probably the most attractive market anywhere in the world for E&P companies to operate." — Dr. Paul Clarke, CEO and President8

In a recent interview with ValueTheMarkets, Clarke also walked through the single-well economics, the JV timeline, and the 12 to 18 month milestone roadmap in detail.

CanCambria is a pre-revenue company at an early stage of development. Investors should weigh the potential scale against the material risks of a company that has not yet established commercial production and remains dependent on securing joint venture funding.

#Global Gas's New Frontiers

The geography of global gas supply has shifted in ways that are structural rather than cyclical. The regions that need the most gas are becoming less able to source it cheaply from where they historically sourced it, and how that tension resolves over the coming decade may well be shaped by investment decisions being made right now, in basins most investors have never heard of.

]]>

")