Scancell (LSE:SCLP)

While vaccine developers Moderna, Astrazeneca and Pfizer have seen significant share price growth since announcing their Covid-19 drug trials, the real opportunity for retail investors appears to be in smaller UK biotechs and biopharmas with significant intellectual property.

Let’s consider Scancell (LSE:SCLP).

The immunotherapies producer recently received a £30 million cash injection from Redmile Group — a US specialist healthcare and life sciences investment fund.

The money will be used to extend the utility of its antibody products and platforms, the company said, as well as to broaden its pipeline of novel therapies and increase funding available for its second-generation Covid-19 vaccine.

The 30% takeover rule

According to the City Code on Takeovers– when a person or group “acquires interests in shares carrying 30% or more of the voting rights of a company, they must make a cash offer to all other shareholders at the highest price paid in the 12 months before the offer was announced.”

That’s because the City treats 30% of the voting rights as effective control of a company.

Redmile Group are at the brink of this 30% ultimate limit — at 29.97%. Scancell’s second-largest institutional shareholder, Vulpes Life Science Fund holds 14.28% of the firm’s shares.

Calculus Capital Ltd is a private equity fund which has invested and exited Scancell several times. This alone might give new investors hope that there is ongoing value in buying in to Scancell for the long term: It retains a 7.9% share in Scancell to date.

The highest price paid for Scancell shares in the last 12 months is 18.35p. But at the point where Redmile decide to take their final few shares, this could be much higher.

So, let’s look at the extra 0.03% that Redmile needs to become Scancell’s buyout contender. With a total outstanding share capital of 791.92 million shares, Redmile would only need to pick up around 240,000 units. At today’s share price of 16p, that means a total outlay of just £38,400.

As we know from the Code, takeovers can mean a big payday for early investors. That’s what some Scancell investors are banking on.

Where Scancell began

Scancell is one of the oldest of this clutch of Covid-19 stocks.

Like many of these small UK biotechs (Scancell has a market cap of £122 million, so it’s not a minnow, but is nowhere near FTSE 250 size, for example), the addition of a potential product to treat Covid-19 alongside its main focus of oncology has swelled investor interest.

The firm was founded in 1997 as a spin-out from Nottingham University with Professor Lindy Durrant at the helm. Durrant is a leader in the field of cancer immunotherapy with a strong track record of taking novel immunotherapies into clinical trials.

In 2006, the company sold its portfolio of antibodies for £4.85 million to AIM-listed Arana Therapeutics. Arana was bought out by NASDAQ-listed Cephalon in 2009, then this parent company was itself taken over by Teva Pharmaceuticals for $6.2 billion in 2011.

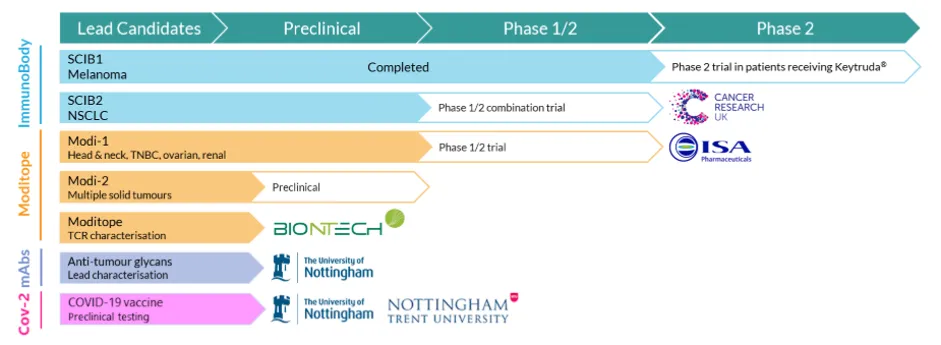

In the intervening time, Scancell had been working on a proof of concept for a novel approach to therapeutic vaccines, a trademarked platform called ImmunoBody.

As with all biotechs and small pharmas, the first barrier to growth is the success of the novel therapies and drugs it is working on. R&D is extremely costly and without significant backing from institutional investors and retail buyers, the company could run out of money before it ever brings a product to market.

However, looking at the current pipeline of clinical trials, the collaboration partners, and the £30 million of cash in the bank, there seems to be sufficient firepower to win the battle on several fronts.

All in the DNA

‘Covidity’ is the codename for Scancell’s DNA vaccine Phase 1 trial, which is expected to start in Q1 2021.

In August, the company received a £2 million grant from Innovate UK to begin a Phase 1 clinical trial. This payout would cover the majority of the company’s costs related to the trial, news releases suggested.

The key point about this DNA vaccine — as opposed to the drugs being developed at warp speed by Astrazenca, Pfizer, and the like — is that it has the potential to provide long-lasting immunity against Covid-19. And crucially, it could protect not only against this strain of the novel coronavirus — SARS-COV-2 — but against new strains of coronavirus that could arise in future.

News out on Friday 6 November 2020 speaks to this point. The Danish government has begun slaughtering its entire population of mink — a relative of the weasel and ferret — because a new mutation of the coronavirus has been found in these animals which are being farmed for their fur.

The Guardian reports remarks by Denmark’s prime minister, Mette Fredericksen, who said the new strain “could pose a risk that future vaccines won’t work”.

As we know, SARS-COV-2 first jumped from animals to humans in the city of Wuhan, the epicentre of the outbreak. Unfortunately, the reality is that there could be many new strains of coronavirus which mutate over time.

As other industry analysts have suggested, the first wave of vaccines released to the public may only be viable to treat 50% of Covid-19 patients, and like the flu jabs that populations now receive annually, may only work for 12 months at most. This is not lifetime immunity.

So, it’s very likely that a second wave — or second generation — of Covid-19 vaccines will become extremely important.

A look at the chart shows Scancell in steady decline from 2016’s peak of 20p, until early July 2020, when it was trading at 5.5p a share. In the three months since, intense investor interest has pushed the price up to 15.5p.

It would certainly be unusual for the pharma industry juggernaut to allow a £120m market cap company to take the prize of a working Covid-19 vaccine. Much more likely, if Scancell’s candidate is proven to work, is that one of the Tier-1 global firms will want the product for themselves.

Any investment in Scancell relies on a series of ‘ifs’. But Scancell is well placed for a number of factors to work in its favour. It’s another one to watch very closely indeed.