Sponsored by: CanCambria Energy. European gas supply remains constrained, with pricing consistently above North American benchmarks. CanCambria is targeting this gap with a large-scale tight gas project in southern Hungary. Access our Exclusive Investor Report on CanCambria Energy.

#Global Gas Prices Show A Wide Regional Split

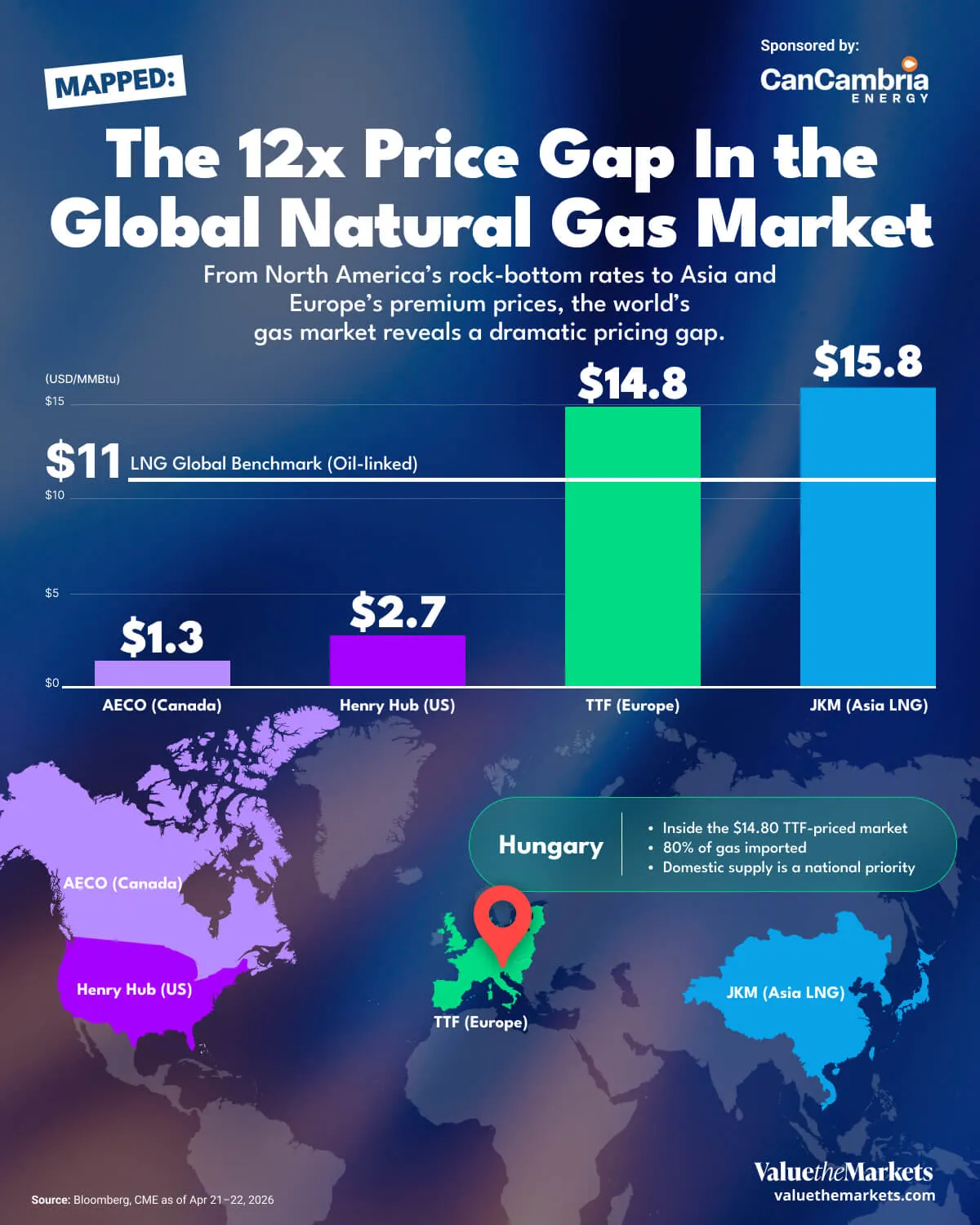

Recent benchmark data shows a global gas market that is still deeply fragmented. As of late April 2026, Henry Hub in the US sits at $2.70 per MMBtu, while AECO in Canada is even lower at $1.30. In Europe, TTF stands at $14.80, and in Asia, JKM is $15.80. Oil linked LNG contracts are estimated around $11 to $13. That vast spread between North American and European benchmarks is not a quirk of seasonality. It reflects a market under structural stress, shaped by a Middle East conflict, constrained infrastructure, and a cargo routing battle playing out across the Atlantic and Pacific basins.

The key takeaway is simple. Gas is not one global price. It is a set of regional prices shaped by pipeline limits, LNG export capacity, storage levels, weather, and contract structure. That helps explain why a producer in Alberta faces a very different market than an LNG seller targeting Asia.

Benchmark | Price | Note |

Henry Hub (US): | $2.70 | Sourced from NYMEX front-month futures1 |

AECO (Canada) | $1.30 | Alberta hub spot2, converted from CAD$1.70/GJ |

TTF (Europe) | $14.80 | Front-month Dutch TTF3, converted from €42.92/MWh |

JKM (Asia LNG) | $15.80 | CME front-month swap linked to Platts JKM4 (~$15.80/MMBtu, Apr 21, 2026), used as proxy for Asian spot LNG |

Oil-linked LNG (global) | $11–$13 | Oil-linked LNG price: calculated from long-term supply contracts where LNG is priced as a fixed percentage of the Brent crude oil price5, not a live market quote. |

Prices approximate as of April 21-22, 2026

#Five Things Investors Should Know

The spread between regions is structural, not seasonal. North American prices are low because production is abundant and export capacity is finite. European and Asian prices are high because those regions depend on imports, and import-dependent markets pay a premium for supply security.

Low North American prices create winners and losers. Henry Hub at $2.70 and AECO at $1.30 weigh on upstream producers with limited pipeline access. But they benefit LNG exporters buying cheap feedgas, gas-fired utilities, and petrochemical producers.

Europe pays a structurally elevated price for imported gas. TTF at $14.80 reflects declining domestic output and a sustained shift toward LNG imports. That premium has been a consistent feature of European gas markets since 2021 and the underlying supply constraints have not been resolved.

Contract structure shapes how benchmark prices translate to earnings. Many LNG deals are indexed to oil rather than spot gas. At $11-13 per MMBtu, oil-linked contracts sit below current TTF and JKM levels, meaning revenue can lag when spot prices spike.

European storage trajectory is a key risk variable. When storage enters winter below the five-year average, the market becomes more sensitive to cold weather. That sensitivity tends to keep prices elevated and volatile through the heating season.

A sharper way to see the markets in just 5 minutes.

Same news, different lens. We cut through the noise and hand you the overlooked ideas and the deeper read the crowd misses. Join 38,000+ investors seeing the markets differently.

#North America Is Oversupplied, Europe Is Not

Henry Hub at $2.70 reflects a market where production is running ahead of export capacity. AECO's deeper discount reflects additional pipeline constraints in Western Canada that directly compress producer margins. That cheap feedgas is precisely what makes North American LNG export projects attractive to buyers in higher-priced markets overseas.

Europe's situation is the inverse. Domestic output has been in structural decline for over a decade. The region has responded by building LNG import capacity and competing on global spot markets. A gas project producing within Europe avoids that import chain entirely, supplying into a market that is structurally short, pays premium prices, and has strong policy incentives to support local production.

#Asia and Oil-Linked Contracts Round Out the Picture

JKM at $15.80 reflects Asia's heavy reliance on imported LNG, with limited pipeline alternatives and less storage capacity relative to demand. Prices are high but more volatile than TTF, driven by weather, shipping constraints, and cargo routing decisions.

Oil-linked LNG at $11-13 sits above North American benchmarks but below current spot levels in Europe and Asia. Because these contracts typically price off Brent with a multi-month lag, sellers do not capture the full upside when spot prices spike. Contract mix shapes cash flow timing and earnings predictability in ways that matter when comparing LNG-exposed companies.

The regional gaps visible in this data reflect years of underinvestment in European domestic supply and growing import dependency across Asia, and they are not expected to close quickly.

#CanCambria Targets Europe’s Gas Gap

CanCambria Energy Corp. (TSXV: CCEC) (OTCQB: CCEYF) (FSE: 4JH) is advancing its 100%-owned Kiskunhalas tight-gas project in southern Hungary, targeting a structurally tight European gas market where domestic supply remains constrained and prices trade well above North American benchmarks6.

The company’s flagship project is built around a large, independently evaluated gas-condensate resource in the Pannonian Basin. Historical wells, modern seismic and legacy production data confirm a proven hydrocarbon system.

CanCambria’s near-term strategy is focused on funding and drilling an initial three-well appraisal program, with first wells targeted for late 2026 and first gas sales expected in early 2027. At US$4/MMBtu, the breakeven gas price for the CanCambria project, compares favorably to the current European gas price.The project benefits from proximity to existing pipeline infrastructure, potentially shortening the path from first flow to revenue if initial results support the development model.

The company has also identified a shallow 350 km² high-impact exploration trend within the Kiskunhalas Concession Area. Multiple leads and prospects have emerged from legacy 2D seismic across a basin that has produced more than 160 million BOE, adding potential lower-cost, faster-cycle upside alongside the deeper tight-gas opportunity.

CEO and President Dr. Paul Clarke commented7:

Hydrocarbon discoveries are commonly made by applying new exploration technologies within proven basins, and that is exactly the opportunity we see emerging at Kiskunhalas.