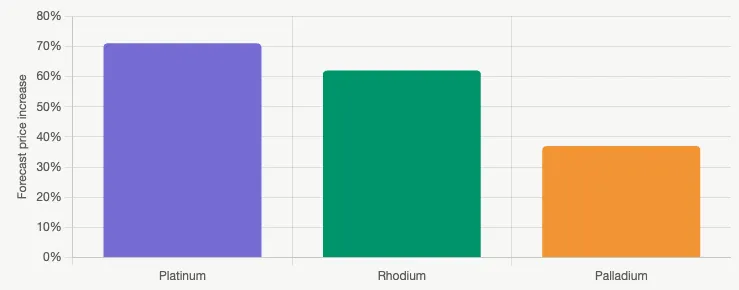

Platinum and rhodium prices are forecast to rise 71% and 62% respectively in 2026, while palladium is projected to gain 37%, consultancy Metals Focus said on Monday1. The London-based firm attributed the divergence to persistent supply deficits across the platinum group metals (PGM) complex.

The forecasts follow a 2025 breakout in the PGM basket price, which moved out of its long-term trading range and lifted producer margins after three years of compression, Metals Focus said. The metals are used chiefly in vehicle exhaust catalysts to neutralise harmful engine emissions.

The expected price gains reflect a basic supply-and-demand imbalance across the platinum group metals market. In recent years, mining output has struggled to keep pace with demand from the automotive, industrial and jewellery sectors, creating persistent supply shortages. Because platinum, palladium and rhodium are produced in relatively small quantities and are difficult to substitute in many industrial applications, even modest deficits can have a significant impact on prices. Higher PGM prices also improve profitability for mining companies, many of which faced squeezed margins during the previous three years of weaker prices and rising operating costs.

#Entire PGM Complex Has Shifted Higher, Swarts Says

"Aside from the Covid pandemic, when we saw sporadic breakouts in these metals, the entire complex has effectively shifted higher," said Wilma Swarts, PGMs director at Metals Focus, in the report. Swarts added that the growth of PGM-free electric vehicles has so far turned out to be less dramatic than expected.

Investment demand, regional dislocations tied to US tariff concerns and tightening physical stocks all contributed to the 2025 breakout, the consultancy said. Compared with a year earlier, platinum, palladium, rhodium and ruthenium are up 110%, 51%, 83% and 158% respectively, according to Metals Focus.

Prices reached multi-year highs in early 2026 before retreating as a gold-led rally faded and the Iran war weighed on investment sentiment, Metals Focus said.

#Lease Rates Signal Continued Physical Tightness

Years of structural supply deficits, meaning the market has been consuming more metal than miners produce for an extended period, are driving tightness across the platinum group metals market. This is visible in elevated London lease rates, the cost traders pay to borrow physical metal for short periods, which remain high following extreme spikes in 2025, Metals Focus said. The spikes were triggered by concerns over potential US tariffs, which prompted traders and investors to move physical metal out of London vaults and into US inventories in anticipation of possible import costs.

Platinum stands out because it benefits from a broader mix of demand sources than other PGMs, including jewellery demand, and because its price tends to move in line with gold, according to Swarts. All PGMs have nonetheless benefited from investor demand for physical assets such as precious metals during a period of heightened geopolitical uncertainty, she said.

Production costs increased in 2025 for major miners in South Africa and Russia, which together account for most global PGM supply, Metals Focus said. Even so, rising metal prices more than offset higher operating expenses, allowing miners to more than double their all-in sustaining cost margins, a key measure of mining profitability that reflects the difference between production costs and realised selling prices, to the highest level in three years.

#Heraeus Sees Reset and Consolidation in 2026

Not all analysts share the constructive view. Heraeus Precious Metals, in its 2026 forecast published in late 20252, said the rally that pushed precious metals to record and multi-year highs "took prices too high too quickly" and projected a period of consolidation through at least the first part of 2026.

Heraeus forecast platinum at $1,300 to $1,800 per ounce in 2026 and palladium at $950 to $1,500, citing a widening palladium surplus as battery electric vehicles erode auto catalyst demand. The firm also said rhodium could transition from a small deficit to a small surplus in 2026, with prices potentially trending lower.

Henrik Marx, head of trading at Heraeus Precious Metals, said in the firm's report that "after such strong price increases, a period of reset and consolidation is likely."

Sustained high oil prices linked to geopolitical tensions involving Iran could also encourage greater EV adoption, as consumers look to avoid rising fuel costs. That trend could further reduce long-term demand for palladium and rhodium in auto catalysts.

#Tariff Resolution and Mine Supply Remain Key Variables

The Metals Focus forecasts depend on several unresolved factors. London lease rates, the fees paid to borrow physical metal in the market, remain elevated, indicating physical supply tightness has not yet normalised, while the resolution of US Section 232 and anti-dumping investigations, trade probes that could lead to tariffs or import restrictions, may shift regional metal flows again, the consultancy said.

Mine supply from South Africa, which accounts for the majority of global platinum and rhodium production, and Russia, a major palladium supplier, remains the largest swing factor for the market. Disruptions such as power shortages, labour disputes, sanctions or weaker mine output could significantly affect global availability. Metals Focus did not provide a tonnage breakdown for projected 2026 supply deficits in the portion of its report cited.

Whether the projected 2026 gains materialise will depend partly on global automotive production volumes, the pace of electric vehicle adoption in major car markets, and the trajectory of the gold price, with which platinum has historically shown a strong correlation. Higher oil prices linked to geopolitical tensions could also accelerate EV adoption over time, potentially reducing long-term demand for palladium and rhodium used in internal combustion engine catalysts, the consultancy said.