Sponsored by: Canterra Minerals. With active drill programs, multiple emerging targets, and recent discoveries, Canterra is advancing a portfolio of copper and gold assets in central Newfoundland. Access our Exclusive Investor Report on Canterra Minerals.

#Why Copper Supply Is Tighter Than It Looks

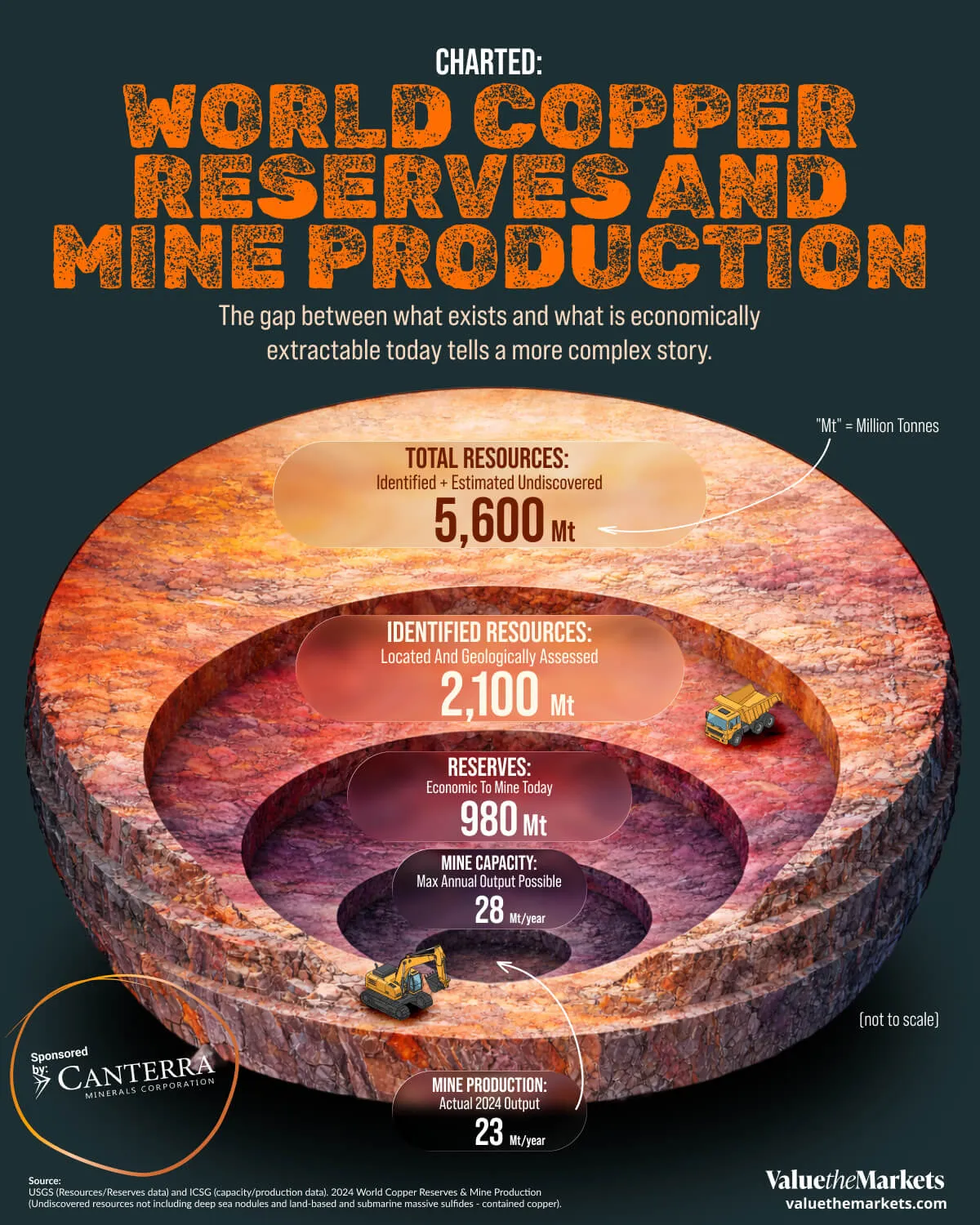

Copper Mining Supply Depends on Reserves, these represent about 980 million metric tonnes (Mt), while identified resources exceed 2,100 Mt, and total resources approach 5,600 Mt. The difference between these categories drives long-term pricing and mining equity performance. Only reserves support mine plans and cash flow today. The rest require higher prices, improved technology, or further development before they become economically viable.

#Why Copper Reserves Are Important For Retail Investors

Reserves drive near term earnings and cash flow

Higher copper prices can convert resources into reserves

Supply growth requires constant capital spending

Long permitting timelines slow new mine development

Electrification trends increase long-term copper demand

Reserves also underpin mine life estimates and net asset value calculations used in equity valuation. If you own mining stocks, you are investing in reserves, not abstract geological estimates.

Layer | Figure |

Total Resources: Identified + Estimated Undiscovered | 5,600 Mt |

Identified Resources: Located And Geologically Assessed | 2,100 Mt |

Reserves: Economic To Mine Today | 980 Mt |

Mine Capacity: Max Annual Output Possible | 28 Mt/year |

Mine Production: Actual 2024 Output | 23 Mt/year |

#The Copper Supply Gap In One Snapshot

The chart shows three very different numbers. About 980 Mt of copper qualifies as reserves. Identified resources exceed 2,100 Mt. Total resources approach 5,600 Mt.

Only reserves are economic to extract under current prices and mining conditions. Identified resources have been discovered and drilled, but include material that may be marginal or uneconomic today. Total resources include both identified deposits and additional copper believed to exist based on geological evidence.

That gap between 980 Mt and 5,600 Mt is the core issue. Copper is geologically abundant. Economic copper is far more limited. For investors, that distinction shapes long-term pricing power and equity performance.

#Supply Looks Large But It Is Price Sensitive

At 23 Mt per year, global mine production is small relative to what sits in the ground. That creates a false sense of comfort. Most of the 5,600 Mt estimated resource base is lower grade, deeper, or located in challenging jurisdictions.

When copper prices fall, companies cut exploration budgets and delay expansion projects. Reserves can shrink as marginal deposits become uneconomic. When prices rise, the opposite occurs. More projects move into the reserve category.

Copper supply expands when prices justify investment and shrinks when they do not. Developing new mines requires exploration, feasibility studies, permitting, and construction, a process that can take a decade or more.

For retail investors, sustained investment in new supply historically requires prices high enough to justify development. Otherwise, supply growth slows over time.

Demand is the other side of the equation.

Global electrification trends increase copper use in vehicles, grids, data centres, and renewable infrastructure.

Copper is not running out. The earth holds substantial quantities. But the portion that is economic today is far smaller than the headline resource number suggests. That distinction underpins long-term copper pricing.

#What This Means For Copper Mining Stocks

For the sector overall, the structure supports a constructive long-term outlook, assuming sustained demand and disciplined capital allocation. Large resource estimates do not cap prices because most of that copper is not economic today. Long development timelines prevent a quick supply response. Electrification in vehicles, grids, and renewable energy systems adds steady demand pressure.

#Structural Tightness Does Not Mean Imminent Shortages

This data does not imply immediate scarcity. It does not guarantee short-term price spikes. And it does not mean every copper junior will succeed.

It supports a thesis of gradual structural tightness. Over time, maintaining supply requires higher incentive prices to convert resources into reserves.

For a retail investor, the edge comes from focusing on reserve quality, cost structure, and jurisdictional risk. Copper’s long-term outlook depends on price-enabled supply. That dynamic favors disciplined producers with durable assets, not marginal projects dependent on perfect conditions.

Against this backdrop, exploration companies play a necessary role in the copper supply chain. If reserves are the foundation of future production, they must first be discovered, defined, and advanced through the resource stage. Companies advancing drill programs in established mineral belts operate at the front end of that reserve replacement pipeline. In a market where long-term supply growth requires ongoing investment and new discoveries, disciplined exploration in prospective jurisdictions represents an early-stage entry point into the reserve replacement cycle that underpins the broader copper thesis.

#Canterra Launches Fully Funded 2026 Drill Program in Newfoundland

Canterra Minerals Corp. (TSX-V: CTM) (OTCQB: CTMCF), a diversified exploration company focused on discovering tier-one copper and gold deposits in the central Newfoundland mining district, recently announced its fully funded 2026 15,000m drill campaign across its 100%-owned projects in central Newfoundland.

The company has uniquely consolidated most of the known copper-gold mineralization in this prolific but historically fragmented region. Its projects are located near historic mines that produced copper, zinc, lead, silver, and gold. Its gold assets lie along a 55 km trend connected to Equinox Gold’s Valentine Mine. Canterra’s position in this emerging district places it early in the exploration cycle, as Newfoundland experiences renewed interest driven by recent high-grade gold discoveries.

Canterra’s 2026 drill campaign includes up to 15,000 metres of diamond drilling split equally across Buchans, the Victoria Lake Supergroup portfolio and Wilding. Its 2,000m winter program at Buchans has already begun following high-grade copper results from Phase 3 discovery drilling reported in November 2025, and high-grade copper intercepts at the Clementine target in September 2025.

Chris Pennimpede, President and CEO of Canterra, commented:

2026 marks the beginning of a true discovery-driven phase for Canterra. At Buchans, winter drilling is already underway as we apply modern deep-seeking geophysics to one of the world’s most prolific high-grade VMS districts and systematically test targets that previous operators could not effectively evaluate at depth.

In parallel, we are advancing our Wilding Gold Project along the same structural corridor that hosts the producing Valentine Mine, where we control a 55 kilometre extension of this gold-bearing trend. Our Q1–Q2 program is designed to refine and prioritize targets ahead of diamond drilling in the second half of the year.

With a fully funded 15,000 metre program and successive drill results anticipated throughout 2026, we believe we are positioned to demonstrate the broader district-scale potential of our Newfoundland land package.